Hims & Hers Health: A High-Stakes Bet on Digital Healthcare’s Future

The telehealth revolution has created both incredible opportunities and devastating pitfalls for investors, and nowhere is this more evident than in the wild ride that has been Hims & Hers Health (HIMS). This San Francisco-based company has transformed from a niche men’s health startup into a billion-dollar telehealth platform that’s reshaping how Americans access healthcare.

But with great growth comes great volatility, and HIMS has delivered both in spades.

After diving deep into the company’s financials, market position, and recent developments, the picture that emerges is one of a company at a critical inflection point. The upside potential remains enormous we’re talking about a company that has grown revenue by nearly 1,700% in five years while pioneering a new model of healthcare delivery.

But the downside risks are equally dramatic, with regulatory challenges, legal battles, and competitive pressures that could derail the entire growth story.

The Upside Story: Why HIMS Could Be a Generational Winner

Explosive Financial Growth That Defies Gravity

Let’s start with the numbers that have made HIMS a Wall Street darling. The company’s revenue trajectory is nothing short of remarkable, showing the kind of exponential growth that usually only exists in Silicon Valley fantasies.

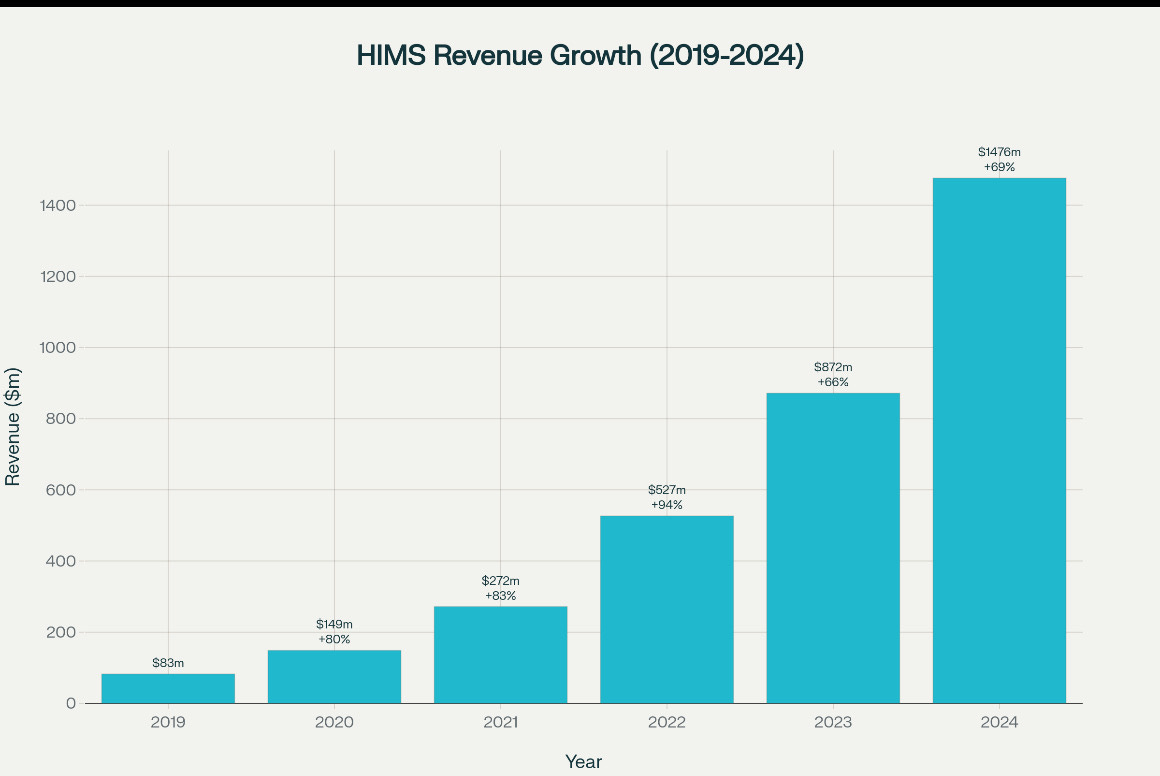

The financial transformation has been breathtaking. From a modest $82.6 million in revenue in 2019, HIMS has exploded to $1.48 billion in 2024 a compound annual growth rate of over 80%. This isn’t just growth; it’s a complete reimagining of what’s possible in healthcare delivery.

But here’s what makes these numbers even more impressive: the company finally achieved profitability in 2024, posting net income of $126 million after years of losses. This milestone represents a fundamental shift from a growth-at-all-costs mentality to a sustainable business model that can generate real shareholder value.

The gross margins tell an equally compelling story. At nearly 80%, HIMS maintains margins that would make software companies jealous. This reflects the inherent leverage in their business model once you’ve built the technology platform and established the provider network, serving additional customers becomes incredibly efficient.

The Subscription Economy Goldmine

What truly sets HIMS apart is its subscription-based revenue model, which has created a recurring revenue machine that’s the envy of the healthcare industry. With 2.2 million subscribers and growing, the company has built a base of customers who pay predictable monthly fees for ongoing healthcare services.

The retention metrics are particularly impressive. According to industry data, 82% of HIMS customers stay on the platform for more than three months, and the company has seen consistent growth in average revenue per user. This creates a compound effect where each new customer acquisition builds long-term value, not just a one-time transaction.

The subscription model also provides remarkable visibility into future revenue streams. Unlike traditional healthcare providers who depend on unpredictable patient visits, HIMS can forecast its revenue with unusual precision.

This predictability is invaluable for planning, investment, and scaling operations.

Market Timing: Riding the Telehealth Tsunami

HIMS has positioned itself perfectly to capitalize on one of the most significant structural shifts in healthcare. The global telehealth market is projected to explode from $123.26 billion in 2024 to $455.27 billion by 2030, representing a compound annual growth rate of nearly 25%.

This isn’t just about convenience it’s about fundamentally reimagining healthcare delivery.

The pandemic accelerated adoption by decades, and consumer behavior has permanently shifted. People now expect healthcare to be as accessible and user-friendly as ordering food delivery or hailing a ride.

The demographics are particularly favorable. Younger consumers, who are more comfortable with digital-first experiences, are entering their prime healthcare consumption years. They’re willing to pay out-of-pocket for convenience and are less tied to traditional insurance-based models.

The GLP-1 Opportunity: A $100 Billion Market

Perhaps the most exciting upside opportunity lies in weight management, particularly GLP-1 medications. The global obesity drug market is projected to reach $73 billion by 2034, and HIMS has positioned itself as a key player in democratizing access to these treatments.

While the company has faced regulatory challenges with compounded GLP-1s, the underlying demand is undeniable. HIMS has demonstrated that it can deliver these treatments at significantly lower costs than traditional healthcare providers, with its $165 monthly pricing competing favorably against $1,000+ monthly costs through conventional channels.

The weight loss offering alone generated over $200 million in revenue in 2024, proving that consumers are willing to pay for accessible, affordable obesity treatments. As the regulatory landscape stabilizes and new partnerships emerge, this could become a massive growth driver.

Technology Moat and Operational Leverage

HIMS has built impressive technology infrastructure that creates meaningful competitive advantages. The company’s AI-powered MedMatch system analyzes millions of data points to optimize treatment plans, creating better outcomes while reducing costs.

The platform handles over 10,000 medical visits daily, demonstrating the scalability of their technology infrastructure. This operational leverage means that as the company grows, its cost per customer acquisition decreases while its ability to serve customers improves.

The company’s plan to scale to 40,000 daily visits shows the enormous growth potential within their existing technology platform. This kind of scalability is rare in healthcare, where capacity constraints typically limit growth.

The Downside Risks: What Could Go Terribly Wrong

Regulatory Earthquake: The GLP-1 Controversy

The most immediate and severe risk facing HIMS is the regulatory firestorm surrounding its GLP-1 compounding practices.

The FDA has made it clear that it views the company’s mass compounding of semaglutide as potentially illegal, and the consequences could be devastating.

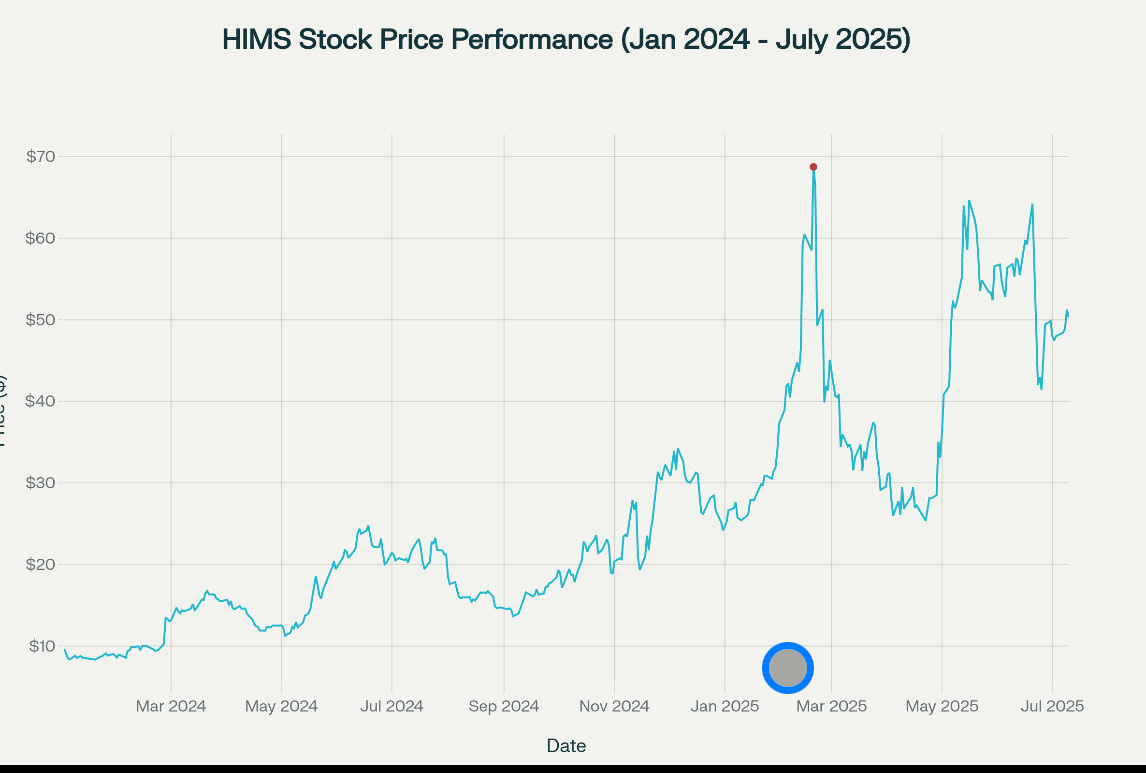

When Novo Nordisk terminated its partnership with HIMS in June 2025, citing “illegal mass compounding” and “deceptive marketing”, it wasn’t just ending a business relationship it was delivering a public rebuke that sent shockwaves through the investment community. The stock plummeted 34% in a single day, wiping out billions in market value.

The regulatory risks extend beyond just financial penalties. The FDA has documented over 100 hospitalizations and 10 deaths associated with compounded GLP-1s, raising serious questions about patient safety. If HIMS is found to have contributed to patient harm through its compounding practices, the legal and reputational consequences could be catastrophic.

Class Action Lawsuits: A Legal Minefield

The regulatory troubles have spawned multiple class action lawsuits that could expose HIMS to massive financial liability. The Sookdeo v. Hims & Hers Health lawsuit, covering the period from April 29 to June 23, 2025, alleges securities fraud and deceptive marketing practices.

If courts find that HIMS deliberately misled investors about the sustainability of its GLP-1 business, it could trigger a cascade of additional legal actions and regulatory scrutiny. The class action deadline of August 25, 2025, represents a critical juncture. The outcome of these lawsuits could determine whether HIMS emerges as a chastened but viable company or faces existential threats to its business model.

Market Valuation Bubble: Expectations vs. Reality

The stock’s incredible volatility reveals a fundamental disconnect between market expectations and business reality. Trading at a forward P/E ratio of over 70, HIMS is priced for perfection in a business that’s inherently imperfect.

The chart tells the story of a stock that has experienced both euphoria and despair. From a peak of $72.98 in February 2025 to recent trading around $50, the stock has demonstrated the kind of volatility that can destroy long-term wealth creation.

With analyst consensus ratings of “Hold” and average price targets of $39.36, representing a potential 22% downside from current levels, professional investors are clearly concerned about the company’s valuation relative to its fundamentals.

Competitive Threats: The Giants Are Awakening

HIMS faces intensifying competition from well-funded rivals with deeper pockets and stronger regulatory relationships. Companies like Teladoc, with its $5.5 billion in revenue and established insurance relationships, represent formidable competition.

The pharmaceutical giants are also entering the direct-to-consumer space. Pfizer and Eli Lilly have launched their own digital platforms, potentially bypassing companies like HIMS entirely. When you’re competing against companies with $80 billion in annual revenue and decades of regulatory relationships, the competitive landscape becomes extremely challenging.

Amazon’s expansion into healthcare, CVS’s digital transformation, and Walmart’s telehealth initiatives all represent existential threats to HIMS’s business model. These companies have the resources to acquire customers at scale and the infrastructure to deliver services more efficiently.

Customer Acquisition Cost Spiral

The company’s customer acquisition costs have risen to $929 per customer, which is concerning in a market where digital advertising costs continue to escalate. For telehealth companies, customer acquisition costs can range from $14 to $61 per patient, but HIMS’s premium pricing reflects the competitive intensity in their target markets.

When larger companies with deeper pockets enter the market, they can afford to outbid smaller players for customer acquisition, potentially making HIMS’s growth model unsustainable. The company’s heavy reliance on digital advertising makes it particularly vulnerable to this dynamic.

Financial Deep Dive: The Numbers Behind the Narrative

Profitability Transformation

The most significant financial development has been HIMS’s transition from consistent losses to meaningful profitability. The company achieved net income of $126 million in 2024, compared to losses of $23.5 million in 2023. This represents a fundamental inflection point in the business model.

The path to profitability reveals important insights about the company’s operational leverage. Sales and marketing expenses, while high at $679 million in 2024, represent a decreasing percentage of revenue as the company scales. This suggests that the subscription model is beginning to generate the compound benefits that make recurring revenue businesses so attractive. EBITDA improvement has been equally impressive, growing from negative $19.9 million in 2023 to positive $79 million in 2024. This operating cash flow generation provides the financial flexibility to invest in growth while maintaining profitability.

Balance Sheet Strength

HIMS maintains a relatively strong balance sheet with minimal debt and substantial cash generation. The company generated $198.3 million in free cash flow in 2024, providing significant financial flexibility for investment and growth initiatives.

The debt-to-equity ratio of essentially zero means the company isn’t leveraged to financial market conditions, providing stability during economic uncertainty. This conservative financial structure has allowed HIMS to weather the regulatory storms without facing liquidity constraints.

Revenue Diversification Analysis

While GLP-1 medications have driven recent growth, the company’s core business excluding weight loss offerings grew 43% year-over-year to over $1.2 billion in 2024. This demonstrates that HIMS has built a diversified revenue base that isn’t entirely dependent on controversial compounding practices.

The company’s five core specialties—sexual health, mental health, dermatology, primary care, and weight management—provide multiple growth vectors and reduce dependence on any single treatment category. This diversification is crucial for long-term sustainability.

Market Position Analysis: David vs. Goliath

Competitive Advantages

HIMS has built several meaningful competitive advantages that differentiate it from traditional healthcare providers. The company’s direct-to-consumer model eliminates insurance complexity, providing a superior customer experience for patients willing to pay out-of-pocket.

The brand recognition in men’s health and sexual wellness creates customer loyalty that’s difficult for competitors to replicate. HIMS has normalized discussions around previously stigmatized conditions, creating a trusted brand that patients turn to for sensitive health issues.

The technology platform’s ability to integrate consultation, prescription, and fulfillment into a seamless experience represents a significant operational advantage. Traditional healthcare providers struggle to match this level of integration and convenience.

Market Positioning Challenges

However, HIMS faces significant challenges in expanding beyond its core demographic. The company’s brand is heavily associated with men’s health, which could limit its ability to capture the broader telehealth market.

The cash-pay model, while providing flexibility, also limits the addressable market to consumers who can afford out-of-pocket healthcare expenses. As economic conditions tighten, this could constrain growth opportunities.

The regulatory scrutiny has damaged the company’s reputation among healthcare professionals and policymakers, potentially limiting partnership opportunities and market expansion.

Our Analysis: What We See Happening

The Regulatory Reckoning

We believe HIMS is facing a fundamental regulatory reckoning that will reshape its business model over the next 18 months. The FDA’s aggressive stance on compounded GLP-1s represents a broader regulatory pushback against what authorities view as regulatory arbitrage.

The company’s future success will depend on its ability to transition from a compliance-skirting growth model to a fully compliant healthcare provider. This transition will likely involve partnerships with pharmaceutical companies, higher costs, and slower growth—but it’s necessary for long-term survival.

The Profitable Growth Inflection Point

Despite the regulatory challenges, we see evidence that HIMS has reached a sustainable profitability inflection point. The company’s ability to generate positive cash flow while maintaining growth suggests that the core business model is sound.

The key metric to watch is the company’s ability to maintain gross margins above 75% while investing in compliance and regulatory relationships. If HIMS can preserve its operational efficiency while addressing regulatory concerns, it could emerge as a stronger long-term competitor.

Strategic Transformation Required

We believe HIMS needs to undergo a strategic transformation from a disruptive startup to a compliant healthcare provider.

This means:

Developing deeper pharmaceutical partnerships

Investing in regulatory compliance infrastructure

Expanding insurance relationships

Diversifying beyond controversial treatment categories

Companies that successfully navigate this transition like Teladoc’s evolution from a niche telehealth provider to a comprehensive healthcare platform can build sustainable competitive advantages.

Investment Thesis: A Binary Bet on Healthcare’s Future

The Bull Case

For investors with high risk tolerance, HIMS represents a compelling bet on the digitization of healthcare. The company has demonstrated that consumers will pay premium prices for convenient, accessible healthcare services.

The total addressable market continues to expand rapidly, and HIMS has built meaningful competitive advantages in customer acquisition and service delivery. If the company can navigate the regulatory challenges, it could emerge as a dominant player in a massive market.

The financial metrics 80% gross margins, growing subscriber base, positive cash flow suggest a business model that can generate substantial returns for shareholders who can tolerate the volatility.

The Bear Case

However, the regulatory and competitive risks are severe enough to potentially destroy shareholder value entirely. The company’s dependence on regulatory arbitrage has created existential vulnerabilities that may be impossible to overcome.

The legal challenges could result in massive financial penalties, and the reputational damage could permanently impair the company’s ability to attract customers and partners. The stock’s volatility suggests that even small negative developments could trigger significant downside.

Our Recommendation

HIMS represents a high-risk, high-reward investment that’s appropriate only for investors who can tolerate substantial volatility and potential total loss. The company’s long-term success depends on successfully navigating regulatory challenges while maintaining its growth trajectory.

For risk-tolerant investors, the current valuation may represent an attractive entry point, assuming the company can resolve its regulatory issues. However, conservative investors should avoid the stock until there’s greater clarity on the regulatory and legal challenges.

The telehealth revolution is real, and HIMS has positioned itself to capitalize on this transformation. But success is far from guaranteed, and the path forward will require skillful navigation of regulatory, competitive, and financial challenges that could make or break the company’s future.

The story of HIMS is still being written, and the next chapter will determine whether this becomes a case study in successful digital healthcare transformation or a cautionary tale about the dangers of regulatory arbitrage.

For investors willing to make that bet, the potential rewards are substantial but so are the risks.

Make sure to always carry out your own research and as always…

Appreciate you