This 37% decline creates a golden opportunity for this equity!

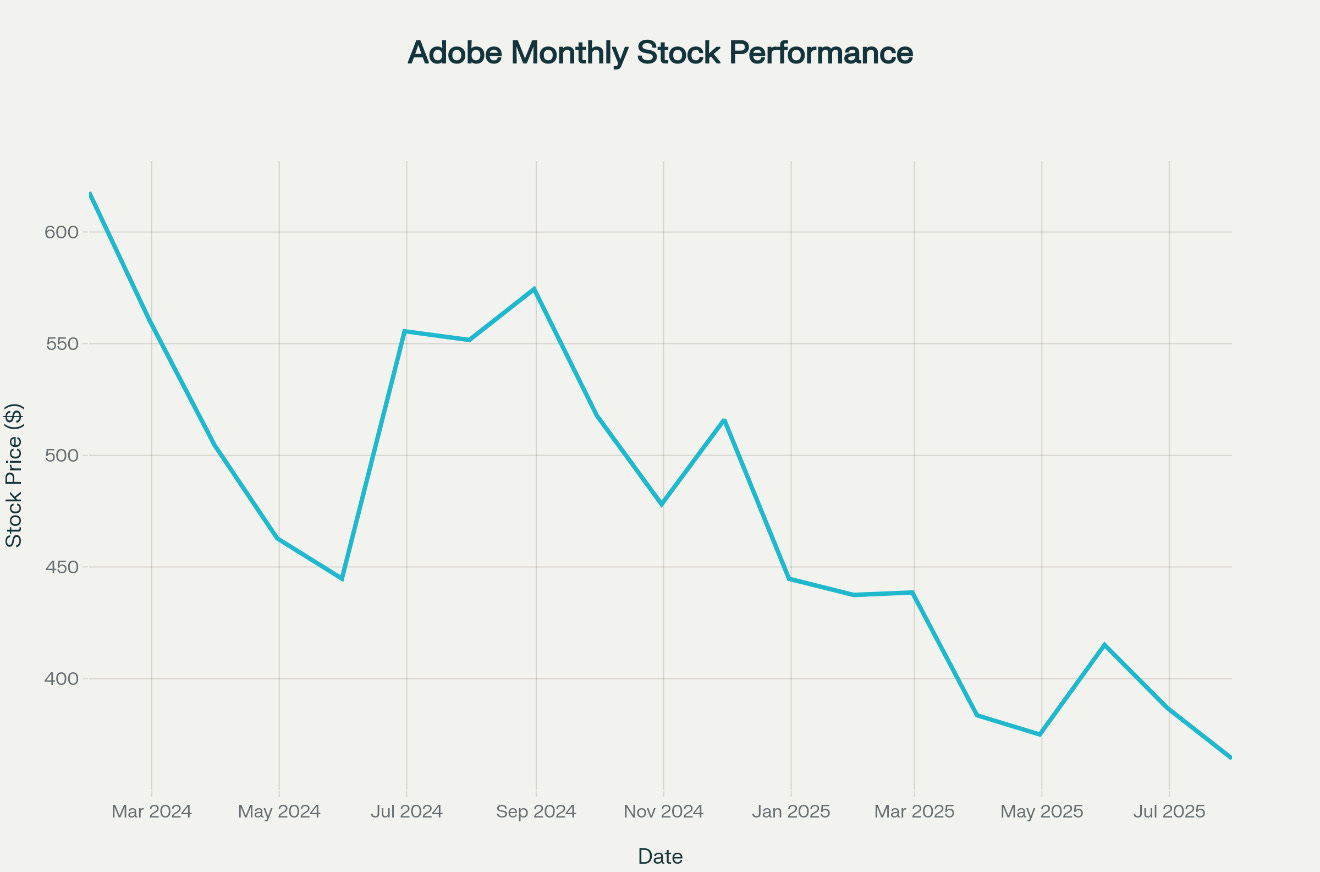

Adobe’s stock has been beaten down mercilessly over the past year and a half, falling from highs of $635 to around $364 – a brutal 37% decline that has left many investors questioning whether the creative software giant has lost its edge.

But here’s the contrarian take: this selloff has created one of the most compelling buying opportunities in big tech today.

While the market has been fixated on short-term headwinds and AI disruption fears, Adobe has been executing a transformation that positions it perfectly for the next decade of growth.

Let’s dive into why this apparent weakness is actually setting up for significant strength.

The Market’s Myopia: Why Adobe Is Being Undervalued

Strong Fundamentals Despite Stock Weakness

The disconnect between Adobe’s stock performance and its actual business results is madness.

In Q2 2025, Adobe delivered record revenue of $5.87 billion, representing 11% year-over-year growth.

The company’s non-GAAP earnings per share of $5.06 beat estimates by $0.09, while operating cash flow hit a record $2.19 billion.

These aren’t the numbers of a company in decline they’re the metrics of a business hitting its stride.

Valuation Becomes Attractive

The stock’s decline has compressed Adobe’s valuation to levels not seen in years.

With a forward P/E ratio of 16.62 and a PEG ratio of 1.09, Adobe is trading at a significant discount to both its historical averages and software sector peers.

Analysts see this disconnect clearly, with an average price target of $484 representing 33% upside from current levels. Some analysts are even more bullish, with DBS setting a $660 target that implies 75% upside potential.

The AI Revolution: Adobe’s Secret Weapon

Firefly: More Than Just Another AI Tool

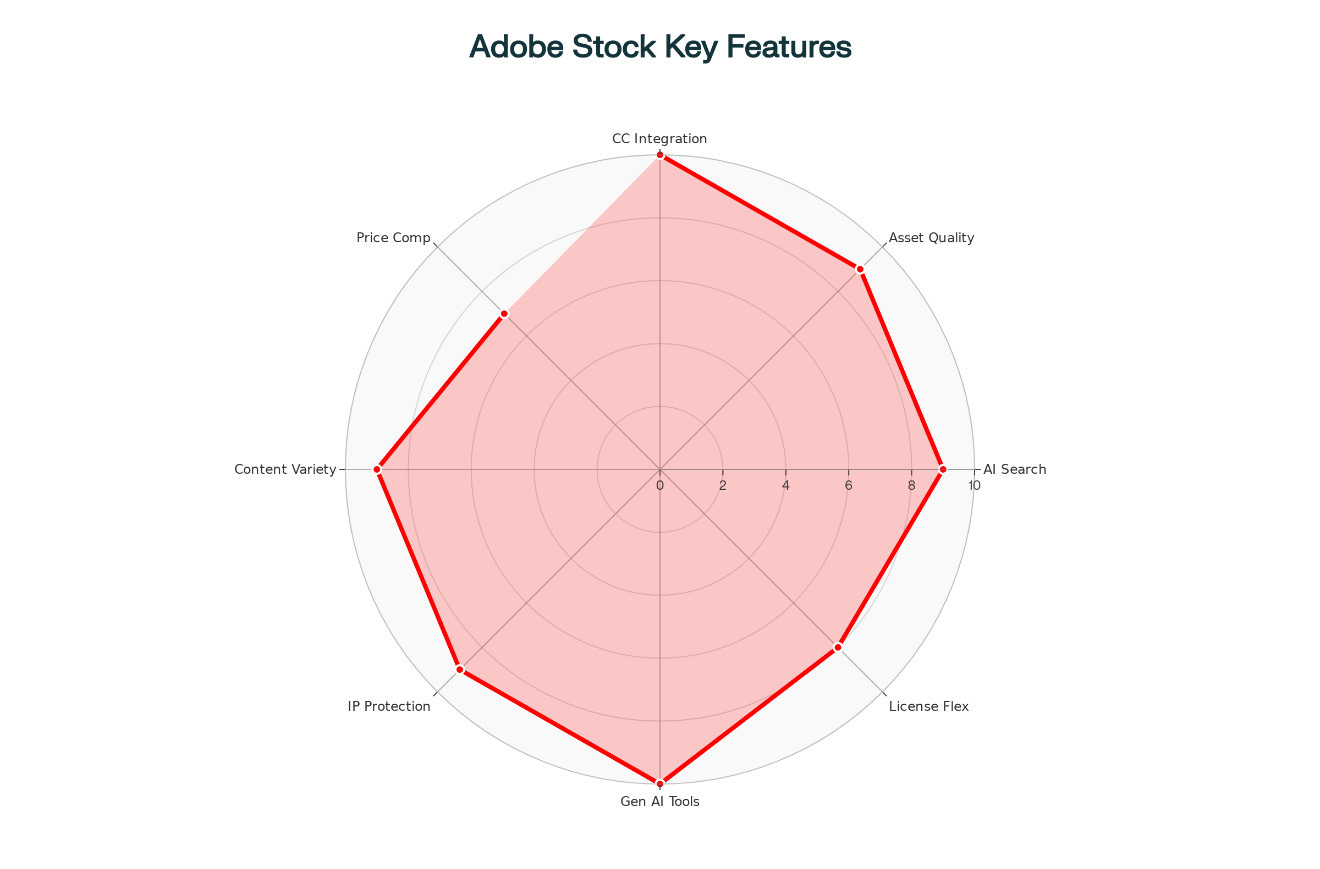

While competitors integrate AI as an afterthought, Adobe has built artificial intelligence into the DNA of its platform through Firefly. This isn’t just about adding AI features it’s about fundamentally reimagining how creative work gets done.

The numbers speak for itself: Firefly has generated over 24 billion assets since its launch, with usage accelerating rapidly. Over 40% of Adobe Express mobile beta users have adopted generative AI features, demonstrating strong user engagement with these new capabilities.

Commercial Safety as a Differentiator

Adobe’s approach to AI training sets it apart from competitors. By training Firefly exclusively on Adobe Stock images, openly licensed content, and public domain materials, Adobe offers something competitors can’t: commercial safety and IP indemnification.

This is crucial for enterprise customers who need legal protection for their AI-generated content.

Revenue Growth Continues Despite Market Concerns

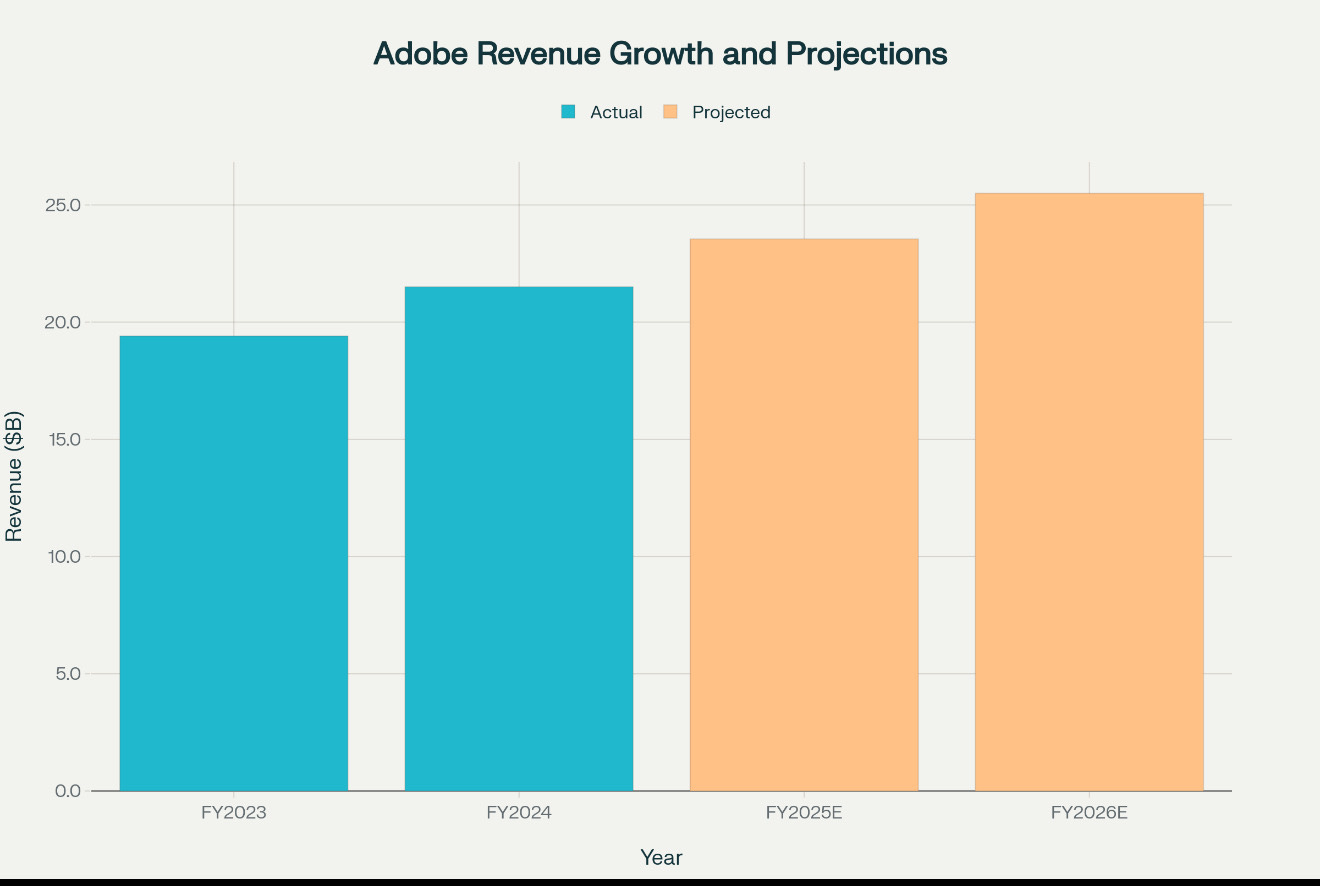

Adobe’s revenue trajectory tells a compelling growth story.

The company has demonstrated consistent growth from $19.41 billion in FY2023 to $21.51 billion in FY2024, with guidance calling for $23.55 billion in FY2025.

Industry analysts project this growth continuing to $25.5 billion by FY2026.

Multiple Growth Drivers Firing

Digital Media Expansion: The Creative Cloud subscriber base has grown to approximately 37 million paid subscribers, adding roughly 1 million new subscribers per quarter. This growth is accelerating as AI features drive both user acquisition and retention.

Document Cloud Momentum: Adobe’s Document Cloud revenue hit $3.18 billion in FY2024, growing 18% year-over-year. The integration of AI Assistant into Acrobat has driven 70% quarter-over-quarter growth in this segment.

Enterprise AI Adoption: Adobe’s enterprise AI solutions are gaining significant traction.

The company’s AI book of business from products like Acrobat AI Assistant, Firefly Services, and GenStudio is tracking ahead of the $250 million ending ARR target for FY2025.

The Competitive Moat Remains Intact

Market Leadership Across Categories

Adobe maintains commanding market positions across its core segments:

Creative Software: Estimated 80% market share with industry-standard tools like Photoshop and Illustrator

Document Processing: Over 90% penetration in Fortune 500 companies with Acrobat

PDF Market: With over 3 trillion Adobe-generated PDFs in circulation

Network Effects and Switching Costs

Adobe’s ecosystem creates powerful network effects. Creative professionals collaborate using the same tools, files are shared in Adobe formats, and workflows are deeply integrated across the Creative Cloud suite. These switching costs have only increased as AI features become more sophisticated and embedded in daily workflows.

Strategic Positioning for Future Growth

Expanding Total Addressable Market

Adobe’s total addressable market is projected to reach $293 billion by 2027, growing at a 13% CAGR. This expansion is driven by:

Broader use cases for creative tools

Increased free-to-paid conversion rates

Enhanced value propositions through AI integration

The company currently captures only about 7% of this projected TAM, indicating substantial room for growth.

Pricing Power Through Value Creation

Adobe recently announced price increases for Creative Cloud, with individual plans rising from $60 to $70 per month and team plans from $90 to $100. The fact that Adobe can successfully implement these increases while maintaining growth demonstrates the value customers place on the platform.

Why Now Is a Time to Buy

Multiple Catalysts on the Horizon

Several factors are aligning to drive Adobe’s stock higher:

AI Monetization Acceleration: AI-influenced ARR is already in the billions and growing rapidly

Market Share Gains: Competitors like Canva, while growing, still represent a fraction of Adobe’s scale and capabilities

Enterprise Digital Transformation: The shift to digital-first business models continues to drive demand for Adobe’s Experience Cloud

Margin Expansion: Operating leverage from AI tools should improve profitability over time

Contrarian Opportunity

The best investment opportunities often come when great companies are temporarily out of favour. Adobe’s current situation simply is strong fundamentals, clear growth drivers, and a depressed stock price creates exactly this type of opportunity.

Our thoughts and analysis

Adobe’s 37% stock decline has created a rare opportunity to buy a dominant technology company at a discount.

The market’s fixation on short-term challenges has obscured the long-term transformation Adobe is executing through AI integration and platform expansion.

With strong financial performance, accelerating AI adoption, and a massive addressable market opportunity, Adobe is positioned to deliver significant returns for patient investors.

The company’s combination of defensive market positions and offensive growth initiatives makes it an ideal holding for the next phase of the digital economy.

For investors willing to look beyond the recent stock weakness, Adobe represents one of the most compelling risk-adjusted opportunities in the software sector today.

The question isn’t whether Adobe will recover – it’s whether you’ll be positioned to benefit when it does.

Thank you all for the support

And as always appreciate you

This analysis is based on publicly available information and should not be considered personalised investment advice. Past performance does not guarantee future results, and all investments carry risk.