Wall Street got this wrong and I’m all in.

AMD just reported what I consider to be one of the most misunderstood quarterly results in recent memory.

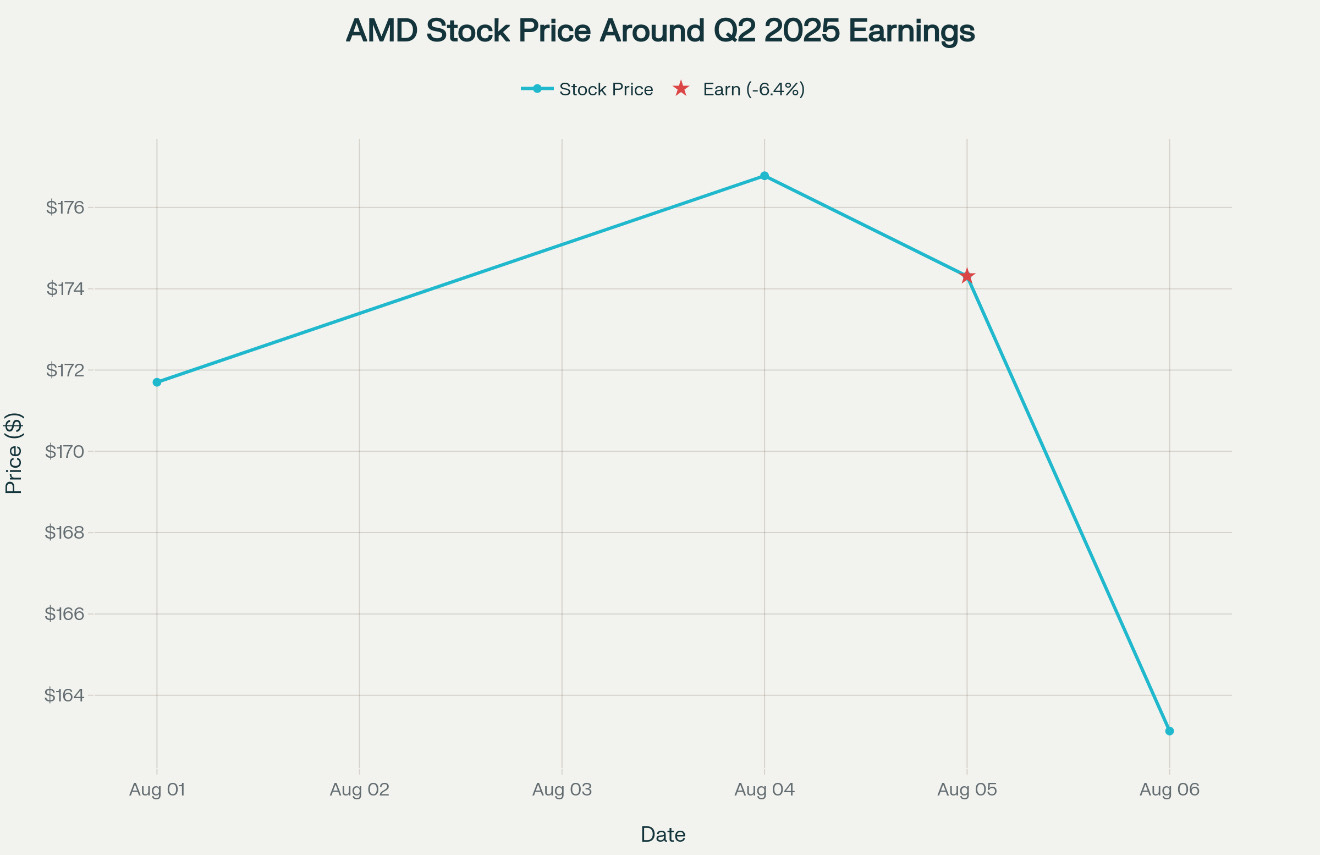

While Wall Street punished the stock with a -6.4% selloff following the August 5th earnings announcement, I believe this reaction represents a classic case of short-term thinking missing the bigger strategic picture.

Here’s why I think the market has it completely wrong.

The Surface-Level Numbers That Spooked Wall Street

Let me start by acknowledging what concerned investors.

AMD reported adjusted earnings per share of $0.48, missing the $0.49 consensus estimate by a penny. The company’s data center revenue growth of 14% year-over-year to $3.2 billion, while solid, paled in comparison to Nvidia’s 73% growth to over $39 billion in the same period.

AMD’s non-GAAP gross margin dropped to 43% from 53% a year ago, primarily due to an $800 million inventory write-down related to U.S. export restrictions on China.

These headline numbers, taken at face value, paint a picture of a company struggling to capitalize on the AI boom while facing geopolitical headwinds.

Wall Street’s knee-jerk reaction was predictable: if you can’t beat Nvidia’s explosive growth, you must be losing the AI race.

But this surface-level analysis misses the fundamental transformation happening beneath the hood.

The Hidden Strengths Wall Street Overlooked

Record Revenue Growth Despite Headwinds

AMD delivered record quarterly revenue of $7.69 billion, beating estimates by $270 million and representing 32% year-over-year growth.

This growth occurred despite the company absorbing significant headwinds from China export restrictions, which CEO Lisa Su indicated would cost approximately $1.5 billion in revenue for 2025.

Think about this mathematically: AMD grew revenue 32% while simultaneously losing what would have been roughly $700 million in Q2 China revenue alone. Without these export restrictions, AMD’s underlying business would have shown even more impressive growth, potentially in the 40%+ range.

Free Cash Flow Explosion

Perhaps the most underappreciated metric in AMD’s results was their record free cash flow generation of $1.18 billion, representing a 168% increase year-over-year.

This isn’t just about profitability it’s about AMD’s ability to self-fund its aggressive R&D investments and strategic acquisitions without diluting shareholders or taking on excessive debt.

Strong free cash flow in a growth phase typically indicates a business model with significant operating leverage potential. As AMD scales its AI chip sales in the coming quarters, this cash generation engine should accelerate further.

The China Export Restriction: Temporary Pain, Strategic Gain

Wall Street treated the $800 million inventory write-down as a permanent impairment, but I view it differently. This represents inventory that AMD can potentially monetize once export licenses are approved or restrictions ease. Recent reports suggest the U.S. government is considering relaxing some AI chip export controls, which could immediately unlock billions in additional revenue for AMD.

More importantly, these restrictions are forcing AMD to accelerate its diversification away from China a strategic positive in the long term.

The company is building stronger relationships with U.S. hyperscalers, European cloud providers, and emerging markets that represent more stable, higher-margin revenue streams.

CEO Lisa Su’s comments on the earnings call were particularly revealing: she emphasized that excluding the China impact, their AI business would have shown significant year-over-year growth, and they’re seeing “tens of billions” in pipeline opportunities.

The AI Chip Market Positioning Wall Street Misunderstands

Critics point to AMD’s relatively modest data center revenue growth compared to Nvidia, but this misses several key dynamics:

The Price-Performance Advantage

AMD’s new MI350 series chips offer compelling price-performance characteristics compared to Nvidia’s offerings. The company recently increased MI350 pricing by 70% to $25,000 per unit while still maintaining a 30% cost advantage over Nvidia’s B200. This pricing power indicates strong underlying demand and differentiated technology.

The Software Ecosystem Is Maturing

One of the biggest knocks on AMD has been their ROCm software ecosystem lagging CUDA. However, recent partnerships with major cloud providers like Oracle, strategic collaborations with OpenAI, and the upcoming ROCm 7 platform release suggest this gap is closing faster than Wall Street realizes.

Market Size Expansion

AMD projects the AI chip market will exceed $500 billion by 2028, growing at over 60% annually. Even capturing a modest market share of this expanding pie represents enormous revenue potential. AMD doesn’t need to “beat” Nvidia—they just need to successfully serve the portion of the market that values price-performance optimization over pure performance.

Valuation: A Rare Opportunity in Expensive Markets

Here’s why I’m treating this selloff as a buying opportunity:

Asymmetric Risk-Reward: At current levels around $163, AMD offers significant upside if they execute on their AI strategy while having strong defensive characteristics from their diversified business model.

Multiple Catalysts Ahead: Q3 earnings in November, potential China export restriction easing, MI350 ramp acceleration, and ZT Systems integration all represent near-term catalysts.

Long-Term Secular Trends: The AI infrastructure buildout is still in early innings, and AMD is well-positioned to benefit from multi-year spending cycles by cloud providers and enterprises.

Valuation Support: Forward P/E ratios in the high 30s/low 40s aren’t unreasonable for a company with AMD’s growth profile and market position.

Conclusion: When Everyone Else Is Selling

The most profitable investment opportunities often arise when there’s a disconnect between short-term sentiment and long-term fundamentals.

AMD’s Q2 results represent exactly this type of situation Wall Street focused on a penny EPS miss and quarterly growth rates while missing the bigger picture of a company successfully diversifying revenue streams, generating record cash flows, and positioning for the next phase of AI infrastructure growth.

I’m not suggesting AMD will match Nvidia’s astronomical returns, but I believe the current selloff has created an attractive entry point for patient investors who recognize that the AI revolution is bigger than any single company and AMD is uniquely positioned to capture a meaningful share of this expanding market.

The Street got this one wrong. The question is whether you’ll join them in focusing on quarterly noise or recognize the long-term signal emerging from one of the semiconductor industry’s most strategic players.

This analysis reflects my personal investment thesis and should not be considered personalized financial advice. Always conduct your own research and consider your risk tolerance before making investment decisions.

Appreciate you as always

Take care